The Ghanaian Parliament has recently debated, voted, and approved a Bill to tax Sugar Sweetened Beverages (SSBs) and other products – as per the Excise Duty Amendment Bill, 2022. My take is: The government and the people of Ghana should not relent, they should get it done to Promote, Protect and Guarantee the Health of Ghanaians, as health costs and deaths linked to diet-related non-communicable diseases (NCDs) mount.

“In this world, nothing is certain but death and taxes” – Benjamin Franklin once said. On ‘taxes’, it is a common refrain in daily conversations of Ghanaians – as they lament “over-taxation”. An associate of mine once noted: “when one makes money, one gets taxed, when one spends, one gets taxed, and when one saves, one gets taxed, do they want us to run out of this country or what?”. As some reporters in Ghana and Kenya have indicated, some consumers have cautioned that, tax whatever you may, but not ‘food’. Can food be taxed? Without hesitation yes, and health-harming food should be heavily taxed if it’s unlawful to outlaw the sale of such foods. Referred to as health taxes, unhealthy foods can be levied. A health tax is a tax, a special kind of tax. In general, health taxes are levied on products that adversely affect health, most notably tobacco, alcohol, non-alcoholic beverages, gambling, and unhealthy foods. Sometimes referred to as “sin tax”, “fat tax,” “soda tax”, or food-related health tax, when levied on food, this policy initiative seeks to curb excessive consumption of foods high in nutrients of concern such as sugars, sodium, saturated fatty acids, and trans fatty acids). Yes, all such are nutrients but nutrient quality (carbohydrate quality, lipid quality, protein quality, etc) are important considerations to make. Excessive intake of these nothing harms health. Therefore, the rationale for a food-related health tax is that if cost/affordability is a significant food choice consideration, then a higher cost on a food item would deter and reduce demand for, and consumption of the food deemed “unhealthy”. Secondarily, revenues from the taxes can be used to fund important health and social protections interventions – such as prevention and treatment programs for harms caused by consumption of such foods or school feeding programs.

On ‘death’, everyone will die at some point, but it should not be from preventable causes, particularly from the foods we eat. Diets – the foods that are consumed, or are recommended to be consumed by humans, were not meant to kill. Detailed during the fourth century (B.C.E), we have the benefit of reading today about what was considered an appropriate diet. Quite recently a group of experts recommended as healthy diets, “diets that are largely consisting of vegetables, fruits, whole grains, legumes, nuts, and unsaturated oils, low to moderate amount of seafood and poultry, no or a low quantity of red meat, processed meat, refined grains and added sugar”. Without a doubt, sugars, particularly in liquid form, but more broadly, SSBs (such as regular soda or soft drinks, fruit drinks, sports drinks, energy drinks, and sweetened waters) are harmful to health. These products can, and should be taxed. The consumption of SSBs is a risk factor for several diet-related NCDs (such as obesity, diabetes, hypertension, cardiovascular disease and many common cancers – according to the World Health Organization and others. On average, a single can of a sugary drink contains up to 40 grams of granulated sugar equivalent to around 10 teaspoons or 10 cubes of table sugar. Few, if any, would fetch 10 or 20 or 30 teaspoons of sugar and gulp it down, and yet many do in the form of SSBs. A friend once asked, “If you will not take 20 cubes or 20 teaspoons of sugar, why take two or three, or four cans of a sugary drink daily”? My response: most of those who do, do not know they are gulping down several cubes of sugar. For more information see Grethe Koen’s Sugar Scale. No one would like to take their money and buy sickness, and yet the consumption of SSBs is harmful to health.

Urgent action is needed to curb the rise of NCDs, as the global NCDs targets that Ghana has endorsed beckons. These targets include the World Health Assembly targets of “halting the rise of obesity and diabetes; reducing premature deaths from NCDs by 25% by 2025; and the Sustainable Development Goals (SDGs) target of “reducing premature deaths from NCDs by one-third by 2030”. Taxes (particularly food-related health taxes such as SSB taxes) have been recommended by the WHO as an effective intervention to reduce the consumption of sugars and other foods implicated in obesity and NCDs. Usually paid at the time of purchase, currently, several countries have enacted and are implementing SSB taxes, which evidence suggests, with some debate, reduces SSBs consumption and generate a good deal of revenue for governments. If ring-fenced or earmarked, the revenue can be applied to address the harms caused by their consumption. Additionally, taxes on SSBs instigate their reformulation by industry. Below a nationally stipulated threshold, reformulated SSBs – SSBs with reduced amounts of sugar may not be taxed.

In Part II, I restate the concerns and requests that the “Advocating for Ghana’s Health (A4H) Coalition” recently submitted to the Government of Ghana, and reassure Ghana’s food environment stakeholders that a food-related health tax is a win-win-win policy – for government, for public health, and for industry.

The writer, “Amos Laar, PhD” is a Professor of Public Health Nutrition at the School of Public Health, University of Ghana, Legon and Principal Investigator (PI) of the A4H Project, the HD4HL Project and the ‘MEALS4NCDs Project’ and Co-PI of the Dietary Transitions in Ghanaian Cities. He is a Fellow of the Ghana Academy of Arts and Sciences.

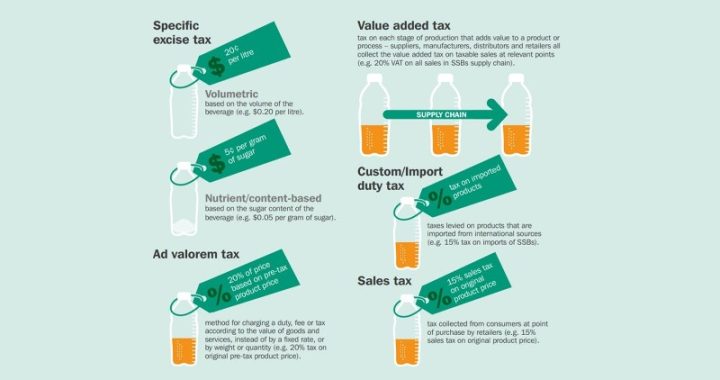

Source of image: Source: World Cancer Research Fund International (2018). Building momentum: lessons on implementing a robust sugar sweetened beverage tax.